Decarbonizing the electric power sector will need massive deployment of clean energy resources, primarily wind and solar. Significant cost declines have led wind and solar to become competitive with fossil sources, but there are critical challenges to overcome for these variable renewable energy (VRE) sources to dominate the electricity generation mix.

The key challenges are speed, integration, and value.

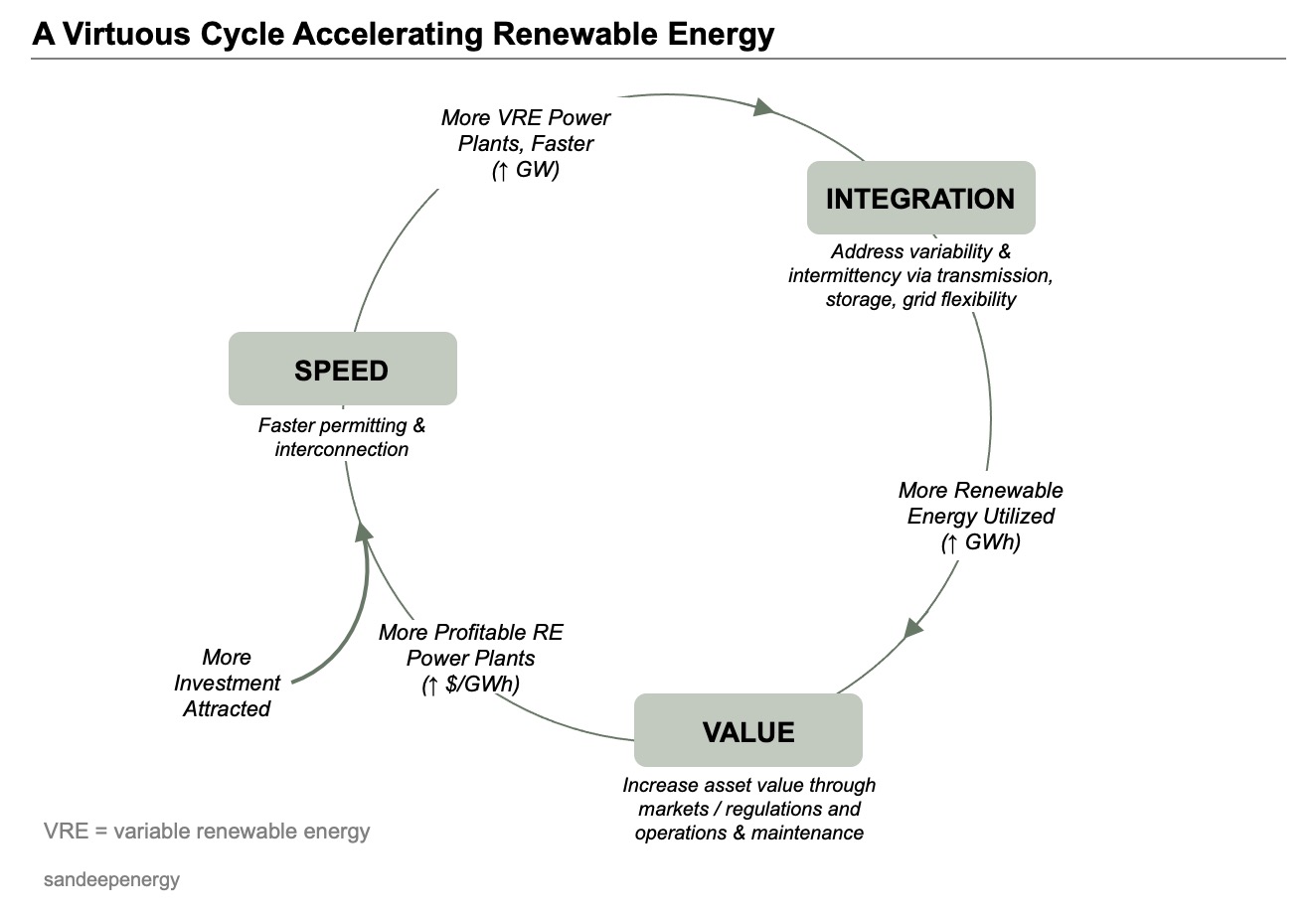

Increasing the pace of deployment, the level of integration in the grid, and further maximizing asset value will create a virtuous cycle accelerating renewable energy and decarbonization.

Speed

The pace of decarbonization needed to limit global warming to +1.5°C or +2°C requires building wind and solar power plants rapidly. However, the permitting process for developing new generation projects can be lengthy and sometimes even kill projects.

Challenges

There are a series of siting, environmental, and grid-related procedures before construction. While necessary, these items can add years to the project timeline and considerable cost. A developer needs to ensure they secure the proper rights to build on a land parcel, that the project’s impact on the local ecosystem is acceptable, and that the plant can connect to the grid. When I discussed barriers to renewable penetration with a public utilities commission member on the integrated resource planning team and a seasoned project developer, both noted that interconnection to the grid is the key challenge:

- State-level Differences: The processes and requirements vary from state to state and can change. Developers need to stay up to speed at the local level in any market they want to compete. This adds overhead to the developer and creates an additional barrier to entry for new developers.

- Interconnection Queue: Utilities need to study the impact of new projects to grid operations & reliability before they can grant access to the transmission or distribution network. There’s a backlog of projects to review, exacerbated by the growing number of applications at both utility-scale and distributed generation.

- Interconnection Cost-Allocation: Many projects require upgrades to the transmission and/or distribution network infrastructure (e.g., lines, transformers). Under “cost-causer” methods, the cost of these upgrades can be billed to the project causing the upgrade, which can sometimes be too expensive for a given developer and kill a project.

Opportunities

Permitting processes are critical in the project development process. Any increase in efficiency and related cost reduction would help deploy more renewable energy capacity, faster.

- Digitalization & Standardization: Process digitalization and document standardization is already underway in many states. Best practices should be shared across states, particularly in addressing the growing distributed generation (DG) segment, which exponentially increases the volume of interconnection applications. Organizations such as Clean Power Research are helping utilities address DG interconnection through web-based application & workflow tools.

- Data Transparency: Effective information sharing can help align actions between developers and utilities, avoiding unnecessary work. For example, with a better understanding of distribution system capacity such as through improved hosting capacity analysis (here’s an example of a hosting capacity map), DG developers can be more targeted with their projects. This can reduce the volume of speculative low-quality applications, thereby reducing utility time spent on reviewing applications, addressing inquiries, and doing feasibility studies. More clarity and certainty on costs would also help. NREL is collaborating with industry to develop tools (e.g., SolarTRACE and SolarAPP) to increase transparency and automation.

Note, other areas for improvement not covered here that can increase deployment speed include system design, sales, financing, and construction.

Integration

Challenges

The variability and intermittency of wind and solar resources create significant integration challenges & costs to deliver power where and when it is needed. As VRE reaches a majority share of the generation mix on a grid, these issues can drive reliability or operational issues.

- Variability: Wind and solar are uncontrollable (or non-dispatchable) resources that are available for power generation based on weather patterns that are different hour to hour, day to day, and so on.

- Intermittency: Output can change unexpectedly and randomly; for example, random cloud cover can reduce solar generation vs. expectation in a given time, potentially impacting grid operations.

- Uncertainty: Compared to dispatchable generators (e.g., natural gas turbines), VRE introduces higher levels of uncertainty, particularly given limitations in more accurate forecasting.

System operators schedule generators to minimize cost while ensuring supply equals demand, transmission lines do not violate capacity constraints, and if a generator does not provide expected supply that other generators can fill the gap. In the current market framework, wind & solar are treated as negative loads, and dispatchable generation is scheduled based on the best estimate of net demand. Net demand with significant VRE on the grid introduces greater levels of uncertainty, which traditionally is addressed by having greater reserve capacity. This approach can drive up system costs and is not an effective strategy for the long term.

Opportunities

We need to be able to integrate greater amounts of VRE into the grid more cost effectively without undoing the sustainability improvement. It doesn’t make sense to overbuild solar & wind capacity and achieve really low capacity factors while addressing intermittency with fast-ramping, carbon emitting natural gas plants. Instead, we need to incorporate:

- Transmission: A lot of solar resources in the US are in the southwest and wind resources are in the middle of the country while the majority of demand is located elsewhere. Long distance high voltage transmission will help connect bountiful generation with cities and dense demand centers. Additionally, a grid covering a larger geographical region can better balance variable resources because weather conditions are more diverse across the pool of resources. Biden’s American Jobs Plan calls for a build out of at least 20GW of high voltage transmission, incentivizing private capital through an investment tax credit. Beyond massive infrastructure construction, this is an area for tech innovation as well. For example, LineVision is deploying advanced sensors and analytics to optimize capacity on existing transmission lines. Veir is developing high temperature superconductor cables with cryogenic cooling to enable very long distance transmission at lower cost.

- Storage: We can time shift renewable supply and help create more firm capacity with energy storage systems. Today, almost all energy storage capacity globally is pumped hydro; however, this approach is geographically constrained. The future grid will employ a combination of hydro, compressed air, thermal, batteries, flywheels, and hydrogen to address various applications. Electro-chemical batteries are a fast growing area given continued cost declines and innovations in increasing energy density. Developers are increasingly adding storage to solar projects. Lithium-ion batteries, such as Tesla’s Megapack are currently best suited for applications within the 4-6 hours range. Companies such as Form Energy are developing new long duration systems that will help time shift energy on the scale of days, weeks, and potentially even seasons.

- Demand Flexibility: The traditional grid paradigm of one-way power following load should change. Advances in sensing, computation, and controls enable load to be shed or time-shifted according to power generation & grid needs. The proliferation of distributed energy resources (DERs) including intelligent & connected HVAC systems, water heaters, electrical devices, electric vehicles, rooftop solar PV, and batteries at the grid edge will significantly increase flexible capacity in the years to come. EnelX and CPower are two of the largest aggregators today in the US, managing load curtailment and delivering economic value for customers from wholesale markets and utility demand response programs. An area I’m particularly excited about, there is a burgeoning tech startup landscape of new entrants that will help usher in a more flexible grid!

Value

Maximizing economic value from VRE assets spurs further investment, construction, and integration. Previous value drivers have included government subsidies (e.g., tax credits), manufacturing-driven cost reduction, and scale benefits. However, as competition increases within renewable energy development, other drivers will require focus & improvement to maintain the healthy returns seen by earlier investors.

Challenges

- Marginal Cost Based Market: Today’s energy market operates on a principle where generators bid into the market based on their marginal cost to provide electricity and system operators schedule generators to minimize total cost. This cost is primarily the fuel cost (e.g., natural gas price) and also includes other variable operational costs. For resources such as solar and wind, the fuel cost is zero, driving a very low marginal cost. Given the market price is set by the last marginal lowest bid generator, VRE should achieve higher prices when the price is set by a fossil-fuel generator and lower prices when VRE supply dominates given demand. As VRE potentially moves to selling more on the merchant market vs. long-term power purchase agreements which give price stability, every incremental MW from VRE in the market depresses the price for the next MW. This represents significant revenue risk in the future.

- Operations & Maintenance (O&M): Optimal plant performance is critical for profit, particularly with potential pricing risk in the future. Asset managers want to minimize downtime and other factors that can limit power output while controlling costs. In a 2018 performance review (see page 4 of SRA2019) by Borrego Solar of 117 solar plants, the main causes of lost generation were soiling due to snow or dirt and inverter issues. With significant mechanical components, wind turbine output and costs can suffer from unexpected or early failures of the blades, gearbox, or generator. With significant component costs and lead times for replacements along with labor costs, wind plant managers cannot afford large failures. As VRE assets mature and significant new capacity is built, the role of O&M will increase in importance and focus.

Opportunities

- Market Design: It’s debatable if the energy market as functioning today can support a VRE-dominated grid and there doesn’t seem to be one clear answer to this complex question. To support the opportunities discussed above in “Integration”, the market needs to adequately compensate and provide price signals to further increase the role of storage and demand flexibility; FERC 2222 is a step in the right direction. There are numerous other considerations including changing bidding mechanisms and driving more real-time trading, removing barriers for VRE participation in different services such as ancillary markets, and somehow strengthening longer-term markets (e.g., PPAs). Experts brought together by Energy Innovation discuss approaches in their 2019 report, “Wholesale Electricity Market Design for Rapid Decarbonization”. The International Renewable Energy Agency published a report on the subject as well - “Adapting Market Design to High Shares of Variable Renewable Energy”.

- O&M - Advanced Sensing, Analytics & Prediction, and Parts & People Management: Asset managers need to use data (electrical, acoustic / vibration, visual, etc.) directly from the equipment and from secondary sensors to find issues before they become bigger (and more costly to fix) or even catastrophic. Data needs to be captured and processed intelligently and fed into analytics models that can predict potential failures. The insights should flow through to systems that manage spare parts, OEM contracts, and labor to effectively, and with a level of automation, manage O&M within the context of broader plant management and market participation.

Create a Virtuous Cycle and Meet Growing Demand

New power plants are built when the existing capacity is not sufficient to meet the demand for electricity. We should expect load growth and aging power plants to retire, creating the need for new power plants.

In developing countries, continued industrialization and growing consumer demand for appliances such as air conditioners should provide significant increase in demand. Across all regions, electrification will lead to increased demand.

While electrification ramps up to create new demand, power plant closure creates necessity. According to Emily Grubert, assistant professor at Georgia Tech, 73% of US fossil fuel generation capacity is due to reach end of life by 2035. It will be key to replace this retiring capacity with clean energy.

Demand will not be the hurdle.

There is clearly great interest amongst the public, capital markets, and some governments in building more renewable energy assets. We will need to solve the problems of speed, integration, and value to maximize and accelerate renewable energy’s future.

- Speed through faster, more effective permitting and processes will get new capacity operational sooner.

- Integration through more transmission, storage, and a more flexible grid will allow for greater utilization of wind and solar resources.

- Value maximization of assets through improved market conditions and O&M increases the profit pool and further drives investment into new renewable energy assets to deploy quickly and integrate into the grid.

Policy, regulation, technology, and business innovation will all be needed to create this virtuous cycle for renewable energy.